Methodology - PDARF

Effective Date: 01/01/2024

Particula Digital Asset Risk Framework (PDARF)

Introduction

The expansion of digital asset markets has created the need for specialized risk assessment tailored to the distinctive characteristics of asset-backed tokens. As institutional allocations to tokenized securities, pegged payment tokens, and natively issued on-chain instruments continue to grow, market participants require analytical tools specifically designed to evaluate the unique combination of structural, legal, and technological features inherent in these instruments. Traditional financial markets have developed well-established credit rating methodologies that provide transparent, consistent assessments of debt instruments across issuers, sectors, and jurisdictions. The digital asset ecosystem requires an equivalent, yet distinctly adapted, analytical infrastructure capable of delivering comparable risk assessments while addressing the heterogeneous token structures, evolving legal frameworks, and diverse blockchain implementations that characterize this market.

Asset-backed tokens, whether structured as tokenized representations of traditional financial assets or natively issued on-chain, present a unique combination of familiar and novel risk dimensions. While these instruments share core structural characteristics with traditional securitized products, including dependence on underlying asset performance and reliance on legal frameworks for investor protection, they introduce additional complexities related to smart contract implementation, blockchain network dependencies, and technical governance mechanisms. This dual nature necessitates an analytical framework that combines established structured finance credit assessment principles with specialized evaluation of technology-specific and legal-structural risks unique to tokenized instruments.

The Particula Digital Asset Risk Framework (PDARF) addresses this requirement through a rules-based, quantitative methodology designed to assess the risk profile of asset-backed tokens using observable data inputs and standardized assessment criteria. The framework provides institutional market participants with transparent, structured risk assessments that evaluate token design integrity, legal enforceability, regulatory coverage, reserve adequacy, and operational resilience.

PDARF is built on the principle that tokenization - independent of the type of underlying asset - alters all major product features of an instrument in ways that warrant a distinct approach to risk assessment. Through the integration of smart contract logic, decentralized infrastructure, and programmable transaction rules, tokenized instruments introduce structural, legal, operational, and technological features that distinguish them fundamentally from their traditional counterparts. Whereas conventional instruments rely on centralized intermediaries and established legal agreements, tokenized or natively issued on-chain instruments embed functional terms within code, interacting with blockchain networks and technical components. As a result, the risks associated with asset-backed tokens extend beyond asset credit quality to include vulnerabilities in technical implementation, governance frameworks, and operational resilience of the supporting ecosystem, encompassing smart contract implementation risks, blockchain network dependencies, technical governance structures, and reliance on specialized infrastructure providers. Traditional credit rating methodologies typically focus on the credit risk of the underlying asset or issuer, treating blockchain as a delivery mechanism rather than a product-defining feature. In contrast PDARF recognizes the digitization process as a structural transformation that necessitates a broader, multidimensional evaluation of the token's risk profile and structural integrity.

PDARF employs a methodological approach consistent with the ordinal ranking systems used by credit rating agencies to facilitate relative risk comparison across rated tokens. By applying uniform assessment criteria and mapping outcomes to a standardized risk rating scale, the framework enables cross-instrument comparability and systematic benchmarking across the digital asset ecosystem. This standardized approach allows market participants to quantify, compare, and monitor risk.

The methodological foundation of PDARF is grounded in established structured finance credit analysis principles, which provide proven analytical frameworks for evaluating instruments whose performance depends on underlying asset pool quality, structural credit enhancement mechanisms, and the integrity of legal and operational infrastructure. However, the application of these principles to asset-backed tokens requires recognition of a fundamental transformation introduced by the tokenization process itself.

Framework Overview

Framework Scope

The Particula Digital Asset Risk Framework (PDARF) is designed to assess asset-backed tokens, whether natively issued on-chain or created through the tokenization of existing financial or real-world assets.

The classification and categorization of tokens eligible for assessment are governed by the Particula Digital Asset Classification System (PDACS), which provides a standardized taxonomy for evaluating the economic structure, legal design, and technical integration of digital assets. PDARF does not assess speculative or narrative-driven digital assets. Its scope is limited to tokens that represent identifiable claims, rights, or ownership interests and are backed by, or associated with, verifiable underlying assets.

Eligible Asset Classes include, but are not limited to:

- Financial assets (e.g., bonds, equities, derivatives)

- Commodities (e.g., precious metals, carbon credits)

- Real assets (e.g., real estate, infrastructure)

- Pegged payment tokens (fiat-pegged or asset-pegged)

- Structured or wrapped tokens (e.g., tranches, vault tokens)

Explicitly Excluded:

- Cryptocurrencies (e.g., Bitcoin, Ethereum)

- Speculative or meme tokens lacking defined economic structure

- Utility and governance tokens without asset backing

- Algorithmic or unpegged payment tokens

Framework Design and Methodology

The Particula Digital Asset Risk Framework (PDARF) is designed to provide transparent, consistent, and data-driven risk assessments of asset-backed tokens. Its structure reflects the distinct characteristics of tokenized or natively issued on-chain instruments and is intended for scalable integration into digital asset ecosystems.

PDARF assesses the structural, legal, technical, and operational quality of asset-backed tokens and evaluates the degree to which a token can be redeemed as contractually promised: On time, in full, and in accordance with its defined structure. As such, PDARF is designed to capture risks across a diverse set of dimensions that address the main risk factors that could lead to losses in these instrument types. The framework does not assess the credit quality of the issuer, does not predict the probability of default, and does not incorporate forward-looking assumptions about market conditions or asset performance. Instead, it quantifies observable risk characteristics across counterparty stability, structural design integrity, and underlying asset quality to produce a present-state risk indicator that reflects the token's ability to honor its obligations based on verifiable data at the time of assessment.

PDARF employs an ordinal rating scale from AAA to D that establishes a hierarchical ranking of relative risk quality across assessed tokens. Unlike cardinal measurements that convey precise quantitative differences, ordinal ratings indicate rank order: A token rated AAA exhibits higher quality than one rated AA, which exhibits higher quality than A or BBB. This approach ensures that ratings serve as standardized benchmarks, enabling market participants to compare risk profiles across diverse instruments, issuers, and structures without requiring granular analysis of each individual security.

Assessment Methodology

The framework evaluates asset-backed tokens through a three-layered hierarchical structure. At the foundation are individual risk attributes, which are discrete and measurable factors derived from observable data, such as regulatory licensing status, smart contract audit results, or asset concentration levels. Related attributes are organized into attribute groups that address specific risk themes (e.g., Regulatory and Legal Standing, Token Implementation Design, Credit Quality). These attribute groups are then aggregated within each of the three core pillars: Counterparty Risk Assessment, Structural Risk Assessment, and Underlying Asset Risk Assessment. This hierarchical organization ensures systematic, transparent, and comparable assessments across diverse token types and asset classes.

The framework applies differentiated weighting at both the attribute and pillar levels to reflect the relative importance of each factor in determining a token's ability to meet its contractual obligations. Individual attributes are weighted based on their materiality within their respective attribute groups, while the three pillars are weighted to prioritize underlying asset quality (50%), followed by structural design integrity (30%), and issuer-related risks (20%). This weighting structure recognizes that the quality and custody of underlying assets represent the primary determinant of redemption capacity, while structural and counterparty factors provide essential supporting context for overall risk assessment.

Hierarchical Assessment Structure

The framework employs a hierarchical assessment structure in which each pillar is composed of thematic attribute groups, and each attribute group contains individual risk attributes. Attributes represent discrete, measurable factors based on observable data inputs, such as regulatory licensing status, smart contract governance mechanisms, or underlying asset risk. This structured approach ensures that assessments are systematic, transparent, and comparable across different tokens and asset types.

Within this hierarchy, both individual attributes and the three pillars themselves are weighted according to their relative materiality in determining overall token risk. The framework assigns greater weight to factors that have a more direct and substantial impact on the token's ability to meet its contractual obligations, while accounting for supporting factors that provide additional risk context.

Pillar 1: Counterparty Risk Assessment

The financial stability, regulatory standing, and operational resilience of the issuing counterparty of an asset-backed token determine whether the entity can fulfill its obligations to token holders and maintain the operational infrastructure necessary for the token to function over time. Counterparty-level risks, including insolvency, regulatory intervention, or operational failures, can compromise investor claims and disrupt core token functions, regardless of the quality of the underlying assets or the soundness of the token structure. This pillar evaluates whether the issuer possesses the institutional resilience, legal authorization, and governance frameworks necessary to support ongoing operations and honor commitments to token holders.

Key Assessment Areas:

- Regulatory and Legal Standing: Evaluation of the issuer's regulatory licenses, legal entity structure, and jurisdictional environment.

- Financial Resilience: Assessment of financial stability, audit quality, management capabilities, and track record.

- Operational and Compliance Frameworks: Analysis of risk management practices, business continuity procedures, compliance procedures (KYC/AML), and financial reporting transparency.

Pillar 2: Structural Risk Assessment

Digital assets’ technical implementation, legal protections, issuance structure, economic design, and blockchain infrastructure determine whether the token can reliably execute its intended functions and whether token holder rights are enforceable and protected. Unlike risks stemming from issuer capacity or asset quality, structural risks reside within the token's own design and architecture, including how smart contracts are implemented, how legal rights are defined and enforced, how regulatory compliance is structured, how economic mechanisms operate, and how the token integrates with underlying blockchain networks. Structural deficiencies, such as exploitable smart contract vulnerabilities, ambiguous legal rights, inadequate reserve verification mechanisms, or dependence on unstable blockchain infrastructure, can prevent a token from performing as designed, independent of issuer quality or asset backing. This pillar evaluates whether the token's structural components are robust enough to support reliable operation and enforceable token holder protections.

Key Assessment Areas:

- Token Implementation Design: Evaluation of smart contract security, upgrade mechanisms, access controls, compliance features, and technical governance.

- Investor Protection: Assessment of legal safeguards, bankruptcy remoteness, asset segregation, and enforceability of token holder rights.

- Issuance Structure: Review of regulatory framework, terms and conditions clarity, investor data access rights, and reserve verification procedures.

- Token Economics: Examination of redemption mechanisms, supply management, market dynamics, fee structures, and distribution mechanisms.

- Blockchain Ecosystem: Evaluation of network stability, transaction success rates, finality characteristics, interoperability, and overall technical maturity.

Pillar 3: Underlying Asset Risk Assessment

For asset-backed tokens, the quality and safeguarding of underlying assets represent the source of value and the fundamental basis for meeting token holder claims. The credit quality, composition, and risk characteristics of the asset pool determine the token's capacity to honor redemption obligations under both normal and stress conditions, while custodial arrangements govern whether those assets remain accessible, properly segregated, and protected from loss, misappropriation, or competing claims. Deficiencies in asset quality or custodial safeguards cannot be compensated by issuer strength or structural design features. As such, a token backed by low-quality assets or assets subject to inadequate custodial safeguards is exposed to higher risks in reliably meeting its contractual obligations. This pillar evaluates the credit quality of underlying assets and the operational reliability of custodial arrangements that safeguard those assets.

Key Assessment Areas:

- Credit Quality Assessment: The credit quality of the underlying assets determines the token’s fundamental capacity to fulfill redemption obligations. Deterioration in asset quality, concentration risk, or default events can directly undermine the economic foundation supporting tokenholder claims. This assessment evaluates the credit quality and risk characteristics of the underlying assets based on portfolio composition and quantitative risk metrics. When the token is backed by a fund or asset pool that carries a rating from a Nationally Recognized Statistical Rating Organization (NRSRO), the respective fund rating serves as the primary indicator of credit quality. If the underlying fund or asset pool is not externally rated, a rules-based framework is applied to determine the relative credit risk of the underlying portfolio. This framework incorporates available external credit ratings of individual instruments as proxies for credit quality and supplements them with portfolio-level factors such as concentration, duration, currency mismatch exposure, and asset manager quality. Where the token is not supported by a rated fund or asset pool, the same rules-based approach is used to evaluate the credit quality of the underlying exposure, analyzing risk across multiple dimensions, including proxy credit quality of assets, portfolio concentration, and the liquidity characteristics of underlying holdings.

- Custodian Quality Assessment: Custodial arrangements determine whether underlying assets remain accessible, properly segregated, and protected from loss, theft, or competing claims. Even high-quality assets cannot support redemptions if custodial failures compromise their availability or legal ownership. This assessment evaluates the credit quality and operational reliability of custodial arrangements that safeguard the underlying assets. When the custodian has a credit rating assigned by Nationally Recognized Statistical Rating Organizations (NRSROs), this rating serves as the primary custodian quality indicator. In cases where an external credit rating is not available, a rules-based framework is applied to assess custodian credit quality based on observable characteristics including regulatory standing, operational track record, financial stability, safeguarding procedures, and custodial infrastructure quality.

Scoring Methodology

PDARF applies a rules-based, hierarchical scoring structure designed to ensure consistency, comparability, and transparency across diverse token types. Individual risk attributes are scored based on predefined criteria derived from observable, verifiable data inputs, enabling systematic and objective assessment of discrete risk factors.

Hierarchical Aggregation Structure

The scoring methodology employs a three-layer weighting and aggregation process:

- Attribute Level: Individual risk attributes are assessed based on observable, verifiable data inputs. Each attribute is assigned a score out of 100% according to predefined criteria. The PDARF assesses 129 risk attributes.

- Attribute Group Level: Related attributes are organized into thematic attribute groups. Attributes within each group are weighted according to their relative materiality and aggregated to produce an attribute group score.

- Pillar Level: Attribute groups are aggregated within their respective pillars to determine a pillar-level score. The three pillar scores are then combined to produce the final score and the risk rating.

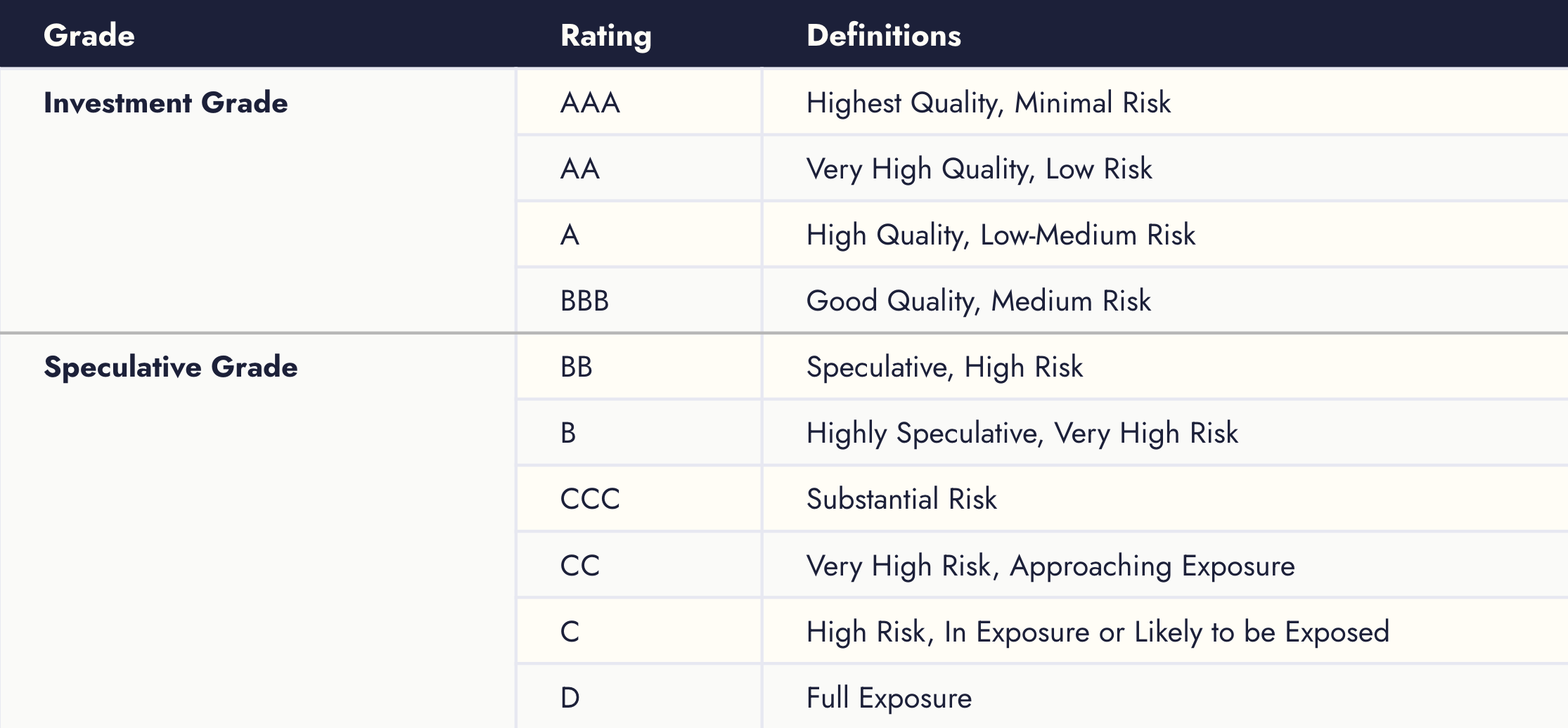

Risk Rating

The framework employs a standardized rating scale ranging from AAA to D, with sub-notches (+/−) available to support additional granularity. This scale enables consistent ranking and relative risk benchmarking across diverse digital assets. The rating scale is defined as follows:

Rating Caps

The framework incorporates rating cap mechanisms for certain critical risk factors. These caps establish maximum achievable ratings when specific structural, operational, or regulatory deficiencies are present, ensuring that fundamental weaknesses cannot be fully offset by strengths in other areas. This approach prevents tokens with fundamental weaknesses from achieving ratings that would misrepresent their underlying risk profile.

Rating caps are applied across the following critical dimensions:

Counterparty Risk Assessment:

- Licensing and Regulatory Accreditation: Evaluates the regulatory authorization, licensing status, and accreditation of the token issuer. Tokens issued by unregulated or inadequately licensed entities face rating caps that reflect the heightened legal and operational risks associated with insufficient regulatory oversight.

Structural Risk Assessment:

- Bankruptcy Remoteness: Assesses the structural integrity of legal mechanisms designed to insulate token holder claims from issuer insolvency. Tokens lacking robust legal segregation of underlying assets are subject to rating caps that reflect exposure to issuer credit risk.

- Token Holder Rights: Evaluates the nature and enforceability of token holder rights to underlying assets. Tokens that confer only contractual claims against the issuer (Relative Rights Token), rather than direct entitlements to underlying assets (Absolute Rights Token), face rating caps that reflect the added marginal risks of higher counterparty risk exposure. Accordingly, tokens lacking a defined claim structure or verifiable asset backing, whether uncollateralized, purely speculative, or narrative-driven, fall outside PDARF's assessment scope and are capped at a risk rating of D (No Claim Token).

- Reserve Verification: Assesses the quality, frequency, and independence of reserve attestation and verification procedures. Tokens without comprehensive, independent third-party verification of underlying asset reserves on a regular basis are subject to rating caps that reflect increased opacity and verification risk.

Underlying Asset Risk Assessment:

- Credit Quality: Evaluates the credit quality and risk characteristics of underlying assets backing the token. Tokens backed by lower-quality, unrated, or high-risk assets face rating caps corresponding to the credit risk inherent in the underlying asset pool.

This approach ensures that fundamental weaknesses in any of these critical areas establish a ceiling on achievable ratings, preventing tokens with material structural, legal, or asset-related deficiencies from receiving ratings that would misrepresent their underlying risk profile.

Data Confidence Score (DCS)

In parallel with the Risk Rating Score, the PDARF framework calculates a Data Confidence Score that measures the completeness and reliability of available information across 199 data points, including the 129 risk-relevant attributes. This score reflects:

- Data availability across all risk indicators

- Consistency and verifiability of disclosed information

- Quality and independence of third-party attestations

- Frequency and timeliness of updates

Higher Confidence Scores indicate greater confidence in the underlying data supporting the risk rating. Lower scores may signal disclosure gaps, inconsistencies, or reliance on incomplete information, which users should consider when interpreting risk ratings. The Confidence Scores provide an independent signal that enables users to contextualize the reliability of associated risk ratings.

Monitoring Mechanisms

To support ongoing risk monitoring, PDARF includes two complementary alert mechanisms:

Trend Detectors: Identify sustained directional changes in a token's risk profile over minimum observation periods. These detectors signal upward or downward shifts based on persistent movements in key risk indicators. Trend detection is descriptive, not predictive. It highlights observed patterns rather than forecasting future developments.

Red Flags: Highlights discrete, high-impact events that exceed predefined risk thresholds. A Red Flag is triggered when a variable exhibits a material deviation, typically exceeding two standard deviations, from recent patterns. While Red Flags do not affect the Risk Rating Score, they serve as supplementary signals to support enhanced monitoring. A triggered Red Flag may indicate the need for closer review or potential re-assessment of risk exposure, particularly when multiple flags emerge across key indicators.

- Counterparty Risk Pillar: Red flags in this category are triggered when material changes occur in attributes including auditor opinions, regulatory licenses and permits as well as KYC/AML framework revisions.

- Structural Risk Pillar: Red flags in this category are triggered when material changes occur in attributes including bankruptcy remoteness, asset segregation, token holder rights enforceability, redemption mechanics, smart contract audit findings, reserve verification, and insurance fund adequacy.

- Underlying Asset Risk Pillar: Red flags in this category are triggered when material changes occur in attributes including portfolio concentration and portfolio duration exposure.

Red Flags serve as early warning signals that complement the core risk rating, particularly when multiple flags emerge simultaneously across key indicators, warranting immediate review and potential risk reassessment.