Navigating U.S. Regulatory Frameworks for Tokenized Fixed Income Products

.png)

Fixed income products are issued within specific legal frameworks that ensure regulatory compliance, protect investors, and optimize tax and operational efficiencies. Each jurisdiction provides distinct structures governed by laws designed to address market stability, investor protection, and capital formation.

.png)

U.S. Investment Company Act Structure

(Issuers for e.g.: Franklin Templeton, WisdomTree)

The Investment Company Act of 1940 is one of the most significant pieces of U.S. financial legislation, establishing stringent requirements for investment vehicles, particularly mutual funds and closed-end funds. The Act was passed in response to the 1929 stock market crash and the subsequent Great Depression, aiming to protect retail investors from risks associated with pooled investments.

- Investment Company Act of 1940: Regulates companies that engage in investing, reinvesting, and trading in securities. This act imposes requirements around disclosure, corporate governance, and restrictions on leveraging (i.e., borrowing)

- Any fund structured under this Act must register with the U.S. Securities and Exchange Commission (SEC) and adhere to strict disclosure rules, including periodic reporting, public filing of fund holdings, and adherence to liquidity standards

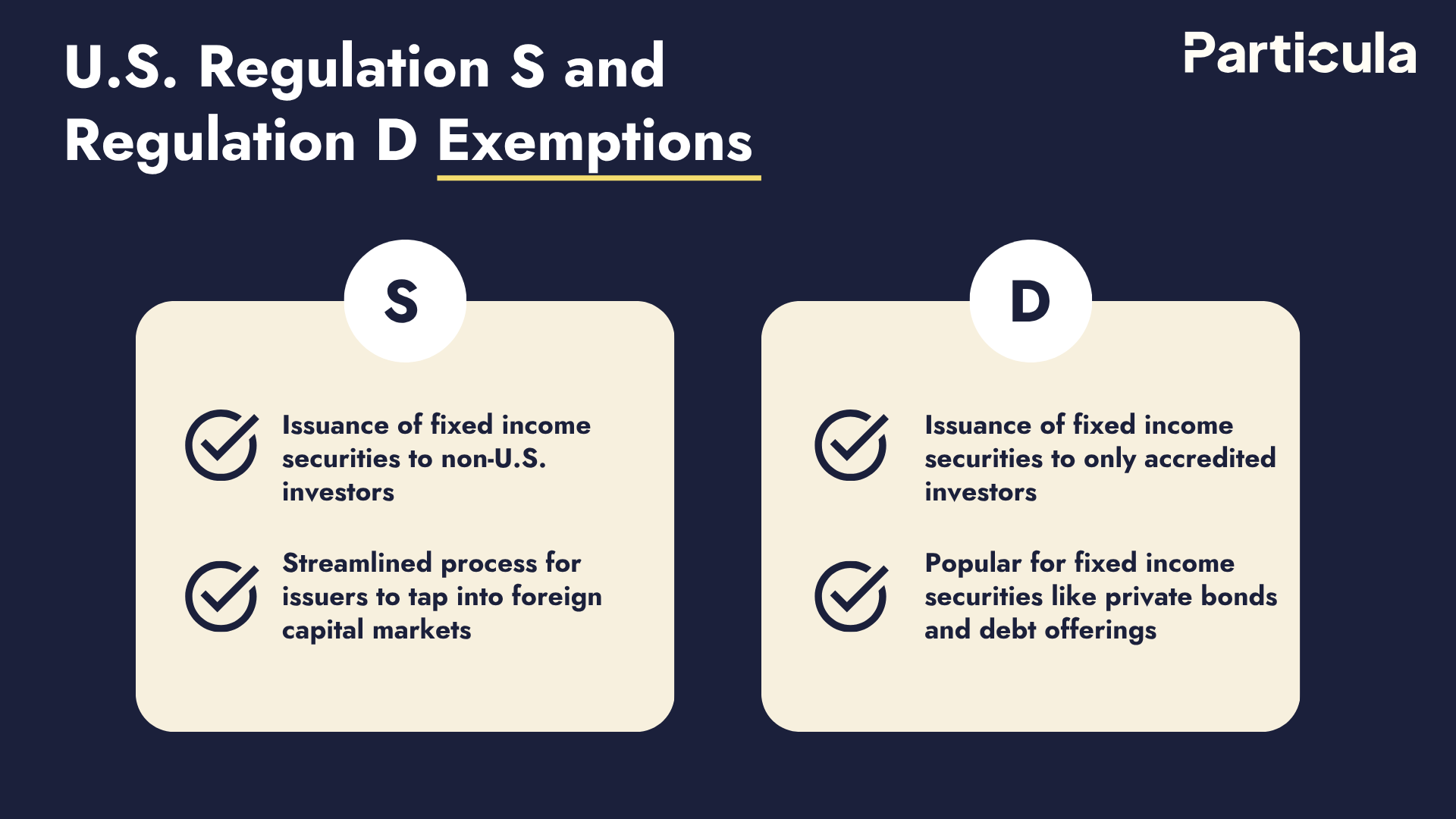

U.S. Regulation S and Regulation D Exemptions

(Issuer for e.g.: Ondo Finance)

The Securities Act of 1933 mandates that all securities offered in the U.S. must be registered with the SEC unless they qualify for an exemption. Two critical exemptions for fixed income products are Regulation S and Regulation D, both of which allow issuers to raise capital without the costs and time associated with SEC registration.

Regulation S

Regulation S, adopted in 1990, allows U.S. and foreign issuers to sell securities to international investors outside the U.S. without SEC registration.

- Securities Act of 1933, Regulation S (1990) provides a "safe harbor" from U.S. registration requirements for offers and sales of securities outside the U.S. This allows for the issuance of fixed income securities to non-U.S. investors without the burden of adhering to domestic U.S. securities laws

- As long as the securities are offered and sold outside the U.S., Regulation S offers a streamlined process for issuers to tap into foreign capital markets

Regulation D

Regulation D, enacted in 1982, offers exemptions for private placements of securities within the U.S., limiting such offerings to accredited investors.

- Securities Act of 1933, Regulation D (1982) allows issuers to offer securities to a select group of accredited investors without registering the securities with the SEC. Accredited investors include institutions like pension funds and individuals who meet certain financial criteria

- This regulation is popular for fixed income securities like private bonds and debt offerings, targeting sophisticated investors who can bear greater risk

U.S. - Delaware Statutory Trust Structure

(Issuer for e.g.: Superstate)

The Delaware Statutory Trust (DST) structure has become a popular choice for issuing structured finance products such as asset-backed securities (ABS) and mortgage-backed securities (MBS). This structure is governed by the Delaware Statutory Trust Act of 1988, codified under Delaware Title 12, Chapter 38.

- Delaware Statutory Trust Act (1988) provides for the creation of DSTs, designed to be flexible and tax-efficient for investors and issuers. The DST allows for the segregation of assets, meaning that the trust’s assets are shielded from the insolvency risks of the sponsor

Assets held in the trust are isolated from the issuer’s balance sheet, providing protection in case of bankruptcy, which is critical in securitization transactions

Use of a U.S. Registered Transfer Agent

(Issuer for e.g.: BlackRock & Securitize)

A registered transfer agent is a critical intermediary in the issuance and management of fixed income products, especially bonds. These entities are regulated under the Securities Exchange Act of 1934, which was designed to restore market confidence after the 1929 market crash by regulating post-issuance securities transactions.

- Securities Exchange Act of 1934, Section 17A mandates the registration of transfer agents with the SEC and outlines their responsibilities. Transfer agents handle the issuance, cancellation, and transfer of securities, ensuring accurate records of bondholders.

- Transfer Agents' role is to facilitate coupon payments, interest distributions, and redemptions for bondholders, ensuring the smooth processing of transactions and compliance with SEC regulations.

Learn More About Particula

At Particula, we have developed the first rating and analytics platform for tokenized assets. Our goal is to provide the next generation of ratings for the next generation of assets in order to give investors instant security, clarity and better market access.

To learn more or gain access to our platform, please contact us at info@particula.io

Latest News & Insights

.png)

Allfunds to Expand Tokenized Funds to Solana, Trusting Particula as Risk Assessment Partner

Allfunds Blockchain today announced it will be expanding its distribution and accessibility of tokenised funds to Solana, a high-performance network powering internet capital markets, payments, AI agents and crypto applications.

.png)

Unlocking Multi-Venue Secondary Markets: GRADE Releases Its Issuer-Venue Eligibility Passport Framework

This paper introduces the GRADE Issuer‑Venue Eligibility Passport (“Passport”), a standardized assessment record: a structured, repeatable framework for evaluating issuer‑venue compatibility across legal, technical, operational dimensions.